Russia – visible disparities in regional growth

April 3, 2019

Many countries in the world are characterized by regional production and growth disparities, both when it comes to advanced and to emerging market countries. Sometimes regional growth statistics may be characterized by good quality, sometimes the quality of officially calculated growth numbers seems to be less illuminating. Regional disparities can also mean different conditions for (foreign) corporate investors what concerns demand and size of the market (for sales), wage levels (for production costs) and educational quality (for access to human resources, better innovation and research and, thus, corporate development).

Regional developments in China and Russia

In China, for example, the addition of all provincial growth results mostly shows higher accumulated economic growth rates than the corresponding weighted numbers for China as a whole. The reason for this discrepancy is frequently explained by better possibilities for the professional promotion of provincial political leaders when good economic results can be shown for the own geographical area of responsibility. Obviously, the central political leadership tries now to change this approach (somewhat), for example by considering environmental improvements as well. However, more exact results in this specific approach still seem to be unknown – at least to me.

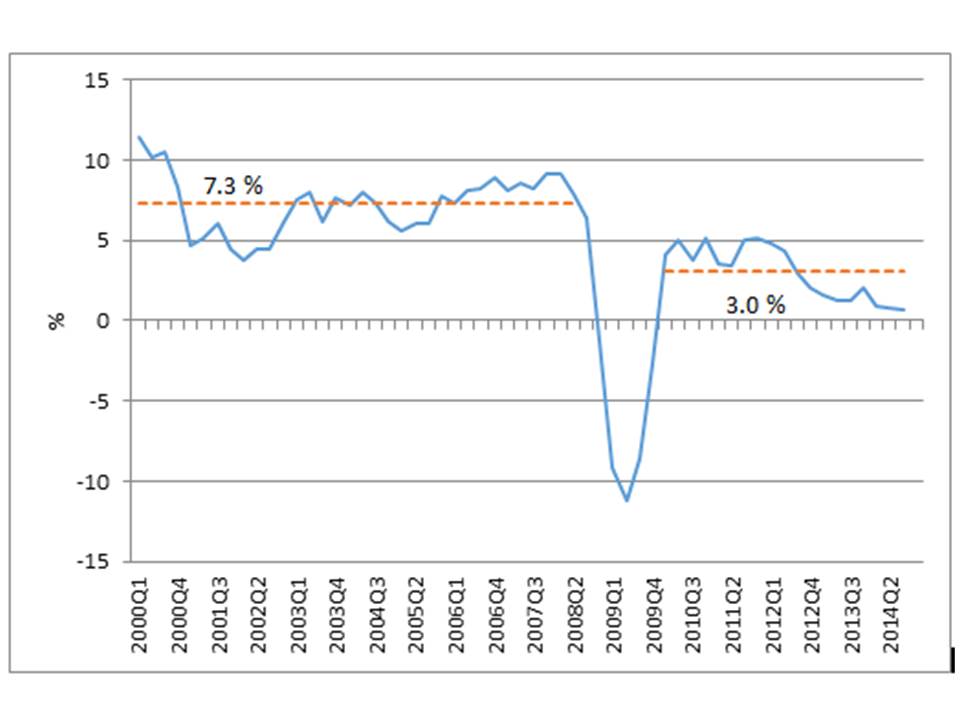

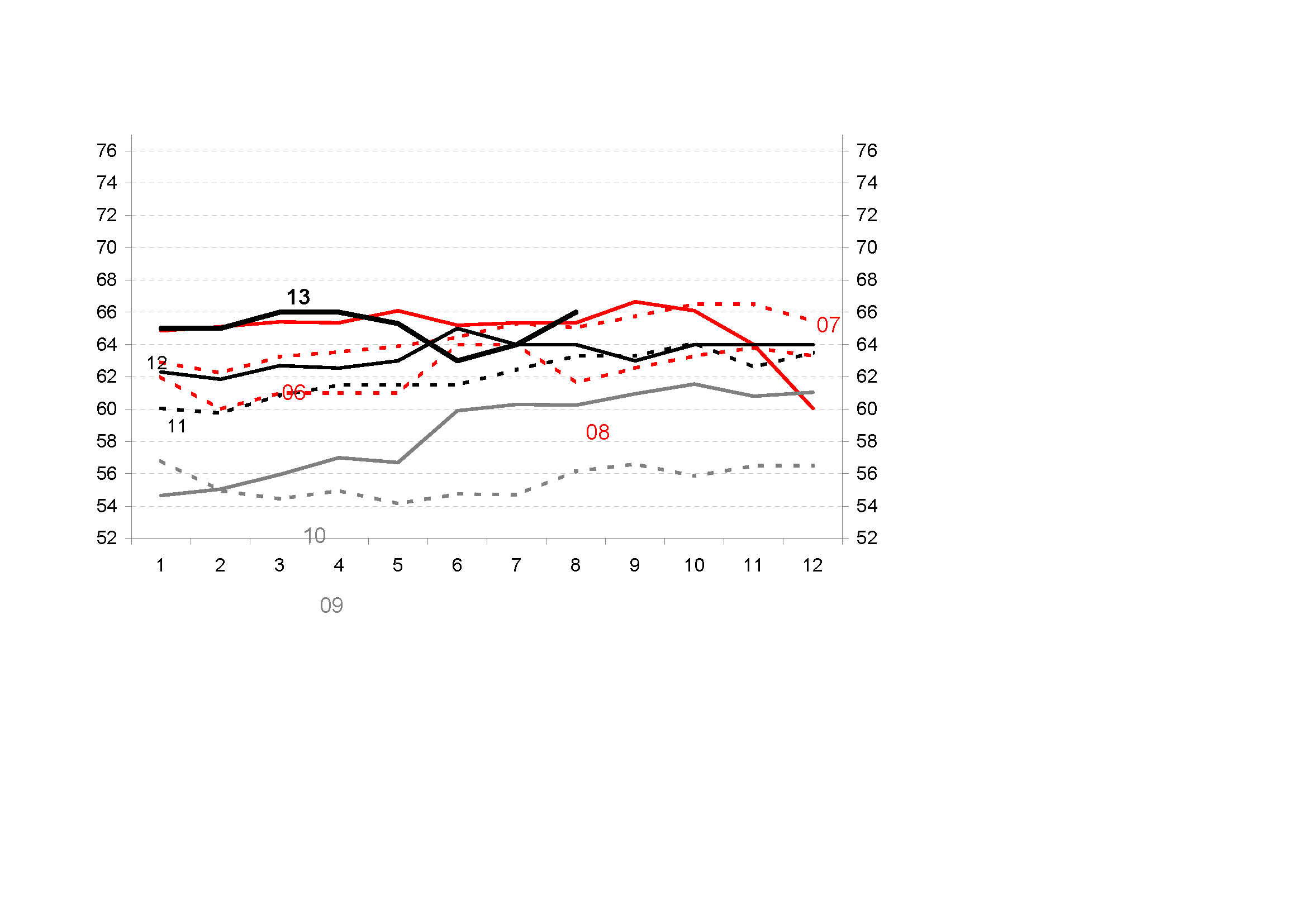

Recently, I found very interesting results for the economic performance of Russian regions, published by BOFIT (The Bank of Finland Institute for Countries in Transition) https://www.bofit.fi/en/monitoring/weekly/2019/vw201913_1/ and originated at the Russian Federal State Statistics Service (Rosstat). The graph published in the link above shows clearly the outstanding positive role of Moscow, the Moscow and the Central region, also compared to St. Petersburg and to the North-West region and even more clearly compared to the Volga and Ural regions. Despite visible improvements in manufacturing production and investments, retail sales still remain sluggish almost over the whole country after the sharp drop in 2015 – with the Moscow region giving a brighter picture also here.

One can also single out by these statistics that the above-mentioned regions counted in 2018 for 81 percent of all Russian manufacturing production and for 70 percent of all fixed investments and retail sales – which certainly can give some guidance for (foreign) corporate planning.

It could be added that BOFIT publishes a lot of interesting news and research, particularly on China and Russia. I never omit their BOFIT Weekly and their other publications. https://www.bofit.fi/en/monitoring/weekly/

Hubert Fromlet

Affiliate Professor at the School of Business and Economics, Linnaeus University

Editorial board