25 years After the Fall of the Berlin Wall – Reflections on Developments in the Former Planned Economies

November 5, 2014

1. On November 9 in 1989, a colleague of mine and I had some meetings in both West Berlin and East Berlin. In the morning, we had no idea about what a few hours later could be called an historical day. We saw the fall of the Berlin Wall with our own eyes. What an event!

This particular experience convinced me pretty soon that it would be worth-while dealing as early and as much as possible with the commenced /forthcoming political and economic revolution that was about to happen.

2. The first country I visited was Poland. This happened already in early 1990. After this trip, I continuously and repeatedly went to all the other countries that were transforming their planned economy into a market system. These early trips to Poland, Czechoslovakia, Hungary and also to the new Baltic states gave me a real feeling of how badly the old system of he planned economy had worked – but also about the enormous efforts that had to be made in order to establish a new, functioning economic and legal system. Somewhat later, Romania, Bulgaria, Slovakia and Croatia, for instance, became interesting places to look at as well.

3. The implementation of the new legal and institutional framework was particularly difficult in the European reforming countries. Reflect, for example, for a few moments how many new – democratic and market-oriented – laws had to formulated, approved by parliament, and finally be applied by the courts! Do not forget all the education of judges that was needed!

The marketization of the planned economies was certainly not easy – and all the administrative/institutional reforms not either. Marketization also included important elements like free competition (whenever appropriate), the establishment of a modern financial system, new monetary and exchange rate policies, the creation of new economic policy tools, privatization, new tax systems, the opening of trade borders, openness for FDI and the import of technology, the encouragement of SMEs, etc. There were indeed mountings of reform areas.

4. Reforming countries with EU-membership objectives proved – generally spoken – be more successful during this transition process than countries without this final goal. Reform pressure – both economically and politically – for joining the EU was sometimes quite tough and had to be managed smoothly.

5. However, despite all the progress in most former command economies: many reforms/structural improvements still have to come (like, by the way, in most of the traditional OECD countries)! All the former planned economies have become part of the global economy. In this context, I would like to quote the late Nobel Prize winner Paul Samuelson who said to me in the 1990s “that globalization means that there is no room anymore for comfortable ineffectiveness”. Certainly not for the previously planned economies either!

It should also be mentioned that most of the (formerly) reforming countries had their ups and downs during the transition process – a transition process that certainly is not yet concluded in all former planned economies in Northern, Eastern, Central, South Eastern European countries – and even less in the nowadays independent Asian countries that previously were parts of the Soviet Union.

6. We have seen during these 25 years how some reform-delayed countries could catch up quite nicely at a later stage – but also the opposite, i.e. how countries with relatively favorable starting positions violated quite a bit of their initially nice reputation. Russia, Belarus and – more recently – Hungary turned out to be the largest disappointments.

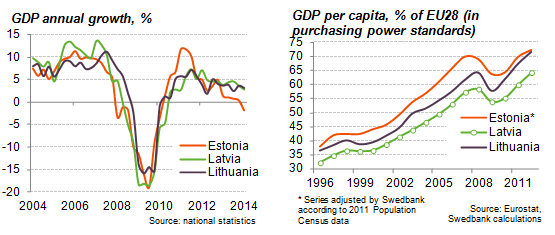

7. The Baltic countries had their ups and downs since the early 1990s. Marketization and most of the necessary institutional reforms went quite smoothly. For a while – in the middle of the past decade – Estonia, Latvia and Lithuania were even called “European tigers”.

Around 2004/2005, however, the Baltic countries became increasingly imbalanced, caused by rapidly growing deficits in the current account and an enormous credit boom which regrettably was backed up strongly by some in the Baltic financial markets dominating and irresponsible Swedish banks. Too passive domestic supervisory authorities and governments made the problem even worse – but also the unilateral strong links to the euro and as a result of this policy the loss of an independent monetary policy. Today, the Baltic countries have achieved a satisfactory macroeconomic balance again – but (potential) growth has come down and problems on the labor market remain in place.

8. Let’s finally come to the economically most successful (reforming) country in the past 25 years (not including the former East Germany in this analysis). In my opinion, the answer is obvious: Poland. I have been many times to Poland in the past two and a half decades and written lots of reports on the country; thus, I do not have any doubt about this conclusion.

9. So what did Poland better than the other reforming countries?

In my view, three special factors were decisive (more, could, of course be mentioned):

¤ the early privatization and the creation of a new financial market

¤ openness to foreign direct investment, and, thus to imports of technology

¤ confidence in Poland’s economy and economic policy – without notable interruption neither domestically nor from abroad. In my view, this confidence part plays an underestimated role in many evaluations of the Polish success story – and should be “administrated” well also by future Polish governments.

Despite this positive general judgment, it should be stressed that also Poland still has a lot of structural work to do: for instance what concerns certain institutions, government debt, the budget process, health care, other social services and future-oriented research. And we realize these days that not even Poland is immune against all kind of external distortion. Russia’s current problems and EU’s disappointing growth development will probably lead to a slowdown of Polish GDP growth pretty soon.

10. Altogether, many positive developments could be noted in the previously planned European economies. Unfortunately, positive trends are not a homogenous phenomenon in the reforming European/Asian countries as a whole. The achievable growth potential has not been met everywhere in the past in the past 25 years. There are obvious winners and losers. However, both the current winners and losers should remember three obvious conclusions:

– the wise words of Paul Samuelson about comfortable ineffectiveness (see above),

– economic heterogeneity between the countries has been increasing strongly since 1990 – and the winners of today are not necessarily the winner of tomorrow (and vice versa),

– speed is not all when it comes to economic reforms; it may be even more relevant to emphasize the importance of continuously moving forward – and not move backward as Russia currently is doing.

At the end of the day, economic growth and well-being is very much about confidence of the household and corporate sector – both in the short and in the longer run.

Hubert Fromlet

Senior Professor of International Economics, Linnaeus University

Editorial board